Newsletter · May 24, 2026

Weekly Digest 21

Nvidia opens a CPU front with Vera, a $135B IPO wave from SpaceX, OpenAI, and Anthropic hits the market, Lilly's retatrutide resets the GLP-1 ceiling, and Amazon's Trainium quietly closes the gap on Nvidia.

Topics we are tracking

Nvidia Q1 FY27 earnings

Source: CNBC — Nvidia (NVDA) earnings report Q1 2027

Nvidia reported another blowout quarter this week. Revenue $81.6B (+85% YoY, +20% QoQ), gross margin 74.9%, dividend raised from $0.01 to $0.25. Q2 guide of $91B at the midpoint implies +95% YoY and +12% sequential. NVIDIA the stock fell 1.77% on May 21 to close at $219.51, then fell another 2% on May 22. This is the fourth consecutive earnings beat that produced a negative tape reaction. The stock is up 19.83% YTD and trading at a $5.4T market cap.

The most important strategic disclosure on the call was the Vera CPU framing. Kress said Vera "opens a brand new $200 billion TAM for Nvidia, a market we have never addressed before" and that Nvidia expects $20B in CPU revenue this fiscal year, "setting us up to become the world's leading CPU supplier." The first Vera racks were hand-delivered last week to OpenAI, SpaceX, Anthropic, and Oracle. Vera is ARM-based, 88 custom Olympus cores, claimed 1.5x performance per core, 2x performance per watt, and 4x density per rack against x86 alternatives. This is Nvidia explicitly opening a second revenue pillar that does not depend on the GPU training cycle and going directly into a market that Intel and AMD have shared between them for two decades.

The read-throughs are clear. The CPU expansion is positive for ARM as the underlying architecture, with the caveat that Nvidia's scale as a customer means the royalty rate will be materially below ARM's standard rate. The implication is mixed for Intel and AMD, where the broader CPU TAM expansion is supportive of both names but the share-loss concern compresses the bullish read. Separately, Huang's dismissal of LPX and SRAM-based accelerators as "niche" is negative for Cerebras, where the entire architectural premise rests on wafer-scale SRAM as an alternative to HBM-bound GPUs. The dominant incumbent rejecting the architectural alternative removes one of the category bull theses.

Data-center CPU market: 2025 → 2028E

Intel (Xeon)

AMD (EPYC)

ARM-based

The China line was the other significant piece of commentary. Q2 guidance assumes zero data-center compute revenue from China. The $4.5B H20 inventory write-down stays at baseline. Huang attended the Trump Beijing summit on May 14, six days before the print, and the visit produced no breakthrough on H200 export licenses. Reuters reported Alibaba, Tencent, ByteDance, and JD.com received Commerce Department approvals to purchase H200s, but US trade representatives confirmed chip export controls were not discussed in the talks. Nvidia is now operating under a 15% US revenue-share framework for any China sales that do materialise. Q1 China revenue was $4.55B against $9.66B a year earlier, a 53% YoY decline.

Further reading:

The IPO race and Anthropic's profitability

Source: SEC — SpaceX S-1 registration statement

SpaceX filed its public S-1 this week disclosing $18.67B in 2025 consolidated revenue and a $4.94B net loss following the February xAI acquisition, targeting a ~$1.75T Nasdaq listing in mid-June. OpenAI confidentially filed its S-1 on May 22 with Goldman Sachs and Morgan Stanley, targeting a Q4 2026 listing at $1T+ against its current $852B private valuation. Bloomberg reported the same day that Anthropic's $30B funding round at $900B is set to close next week, with Sequoia, Dragoneer, Altimeter, and Greenoaks each contributing approximately $2B. Combined new equity supply at announced ranges would exceed $135B, which has no modern precedent.

$135B in new equity supply concentrated in a four-month window creates real absorption pressure. The largest single technology IPO in history was Alibaba at $25B in 2014. SpaceX alone is targeting $75B at a $1.75T valuation, OpenAI is reportedly targeting $60B+, and Anthropic's October listing would add to that. Index inclusion mechanics are the immediate concern: SpaceX at $1.75T would be larger than every company in the S&P 500 combined except Apple, Microsoft, and Nvidia, forcing mandatory buys from S&P 500 and Nasdaq 100 tracking funds estimated at $50B+ on inclusion alone. The marginal source of that capital is selling out of existing mega-cap positions. Liquidity tends to compress in the run-up to and weeks after mega-IPOs as institutional desks reposition. The broader market read is that the second half of 2026 will be defined as much by capital rotation as by AI fundamentals.

Largest IPOs of all time vs. pending H2 2026 mega-deals

The Wall Street Journal also reported that Anthropic told investors Q2 revenue will reach $10.9B, more than doubling Q1's $4.8B, and that the company expects its first operating profit of $559M for the quarter. Last summer the company expected no profitability before 2028. The figure includes training costs but excludes stock-based compensation, and scheduled compute spending later in the year may push the company back into losses on a full-year basis.

The comparison to OpenAI is sharper. OpenAI reportedly generated $5.7B in Q1 2026 against a negative 122% non-GAAP adjusted operating margin, losing $1.22 for every dollar of revenue even excluding stock-based compensation. Per The Information, Anthropic's annualised revenue run rate has reached approximately $45B against OpenAI at approximately $25B. Ramp's May 2026 AI Index, tracking spending across roughly 50,000 US businesses, showed Anthropic at 34.4% of paying business customers against OpenAI at 32.3% — the first crossover since the AI race began, with Claude Code as the primary growth driver.

Further reading:

- Bloomberg: Anthropic to close over $30 billion round as soon as next week

- Capital.com: SpaceX IPO explained

- Ramp: AI Index, May 2026

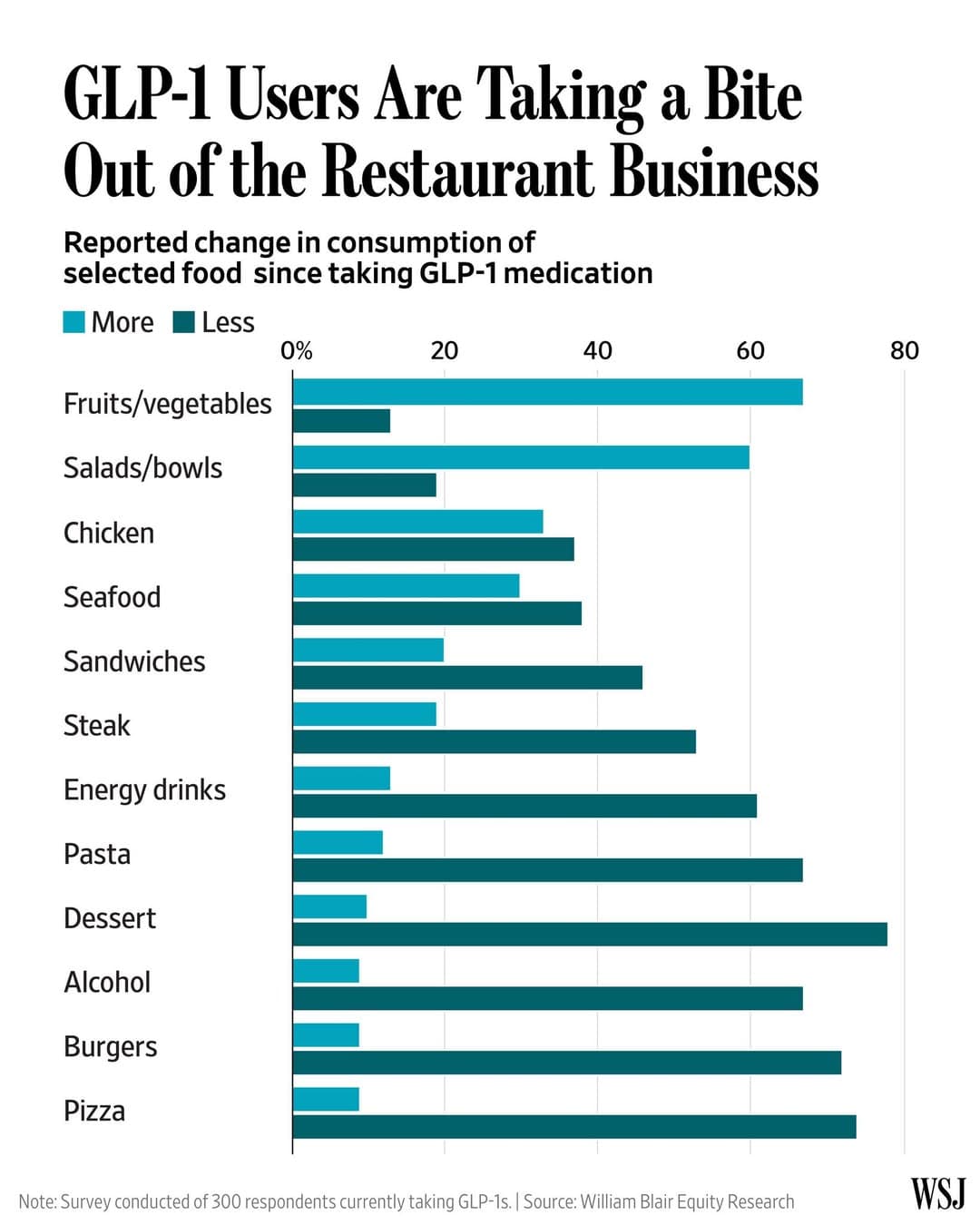

Retatrutide TRIUMPH-1 and the maturation of the GLP-1 cycle

Source: Eli Lilly — Lilly's triple agonist retatrutide delivered powerful weight loss

Eli Lilly reported topline TRIUMPH-1 data on May 21. Participants on the 12mg retatrutide dose lost an average of 70.3 pounds, or 28.3% of body weight, over 80 weeks. 45.3% of the 12mg arm achieved at least 30% weight loss, a threshold historically associated only with bariatric surgery. The 104-week extension in patients with baseline BMI ≥35 reached 30.3%. All doses met primary and secondary endpoints across the 2,339-participant study.

Six more Phase 3 readouts are expected through 2026, covering type 2 diabetes with cardiovascular disease, sleep apnea, knee osteoarthritis, and MASLD. NDA filing is anticipated in late 2026 or early 2027, with launch in 2027 against an installed Zepbound base that gives Lilly the distribution infrastructure to absorb a retatrutide ramp without rebuilding commercial channels.

We continue to believe in the growth of the GLP-1 segment as a whole. Price pressure will be offset by increased usage and adoption. Overweight and obesity have been the largest structural cost burden on global healthcare systems for three decades. A therapy that delivers these kinds of outcomes via weekly injection can reduce that cost burden dramatically. There are also interesting second-order effects on alcohol consumption and sweets consumption that are worth tracking.

Amazon Trainium and the ASIC competition

Source: The Information — Amazon's Nvidia alternative starts winning AI developers

The Information reported on May 19 that Amazon's Trainium accelerators are gaining traction among AI developers who have historically relied exclusively on Nvidia. Customers cited cost savings of up to 35% versus Nvidia H100 on inference workloads. The software gap that long protected Nvidia seems to be narrowing. Google's TPU team used the same playbook when they made TPUs available to external teams and open-sourced many of the software libraries since.

Anthropic has committed up to 5GW of current and future Trainium capacity. OpenAI committed approximately 2GW through the expanded AWS partnership. Teams at OpenAI and Anthropic have no problems getting the maximum out of TPUs or Trainium chips even in the absence of a CUDA-equivalent ecosystem. They have hundreds of the best kernel engineers who can write custom stacks for their models. But the fact that both Google and Amazon are investing more closely in their software offerings shows that they are also interested in making their hardware available to a broader developer ecosystem.

Trainium3 and Trainium4 look very promising in comparison to Google's TPU roadmap. TPU v8 is a technically conservative generation, staying on TSMC 3nm-class nodes rather than advancing to 2nm, and continuing to use HBM3E rather than HBM4. Google's engineering resources went into restructuring the silicon partner model (Broadcom plus MediaTek) rather than into raw performance advancement. This opens a structural lane for Amazon among ASIC developers: Trainium3 is shipping now, Trainium4 has Nvidia NVLink Fusion interoperability built in, and the price-performance trajectory is improving generation over generation. We continue to see Nvidia as the dominant player at the frontier, where execution velocity, the CUDA ecosystem, and the ability to push specs late in the design cycle (Rubin's power and HBM bandwidth upgrades being the most recent example) protect the competitive moat. The interesting question among the ASIC developers is who captures the cost-sensitive inference segment where the CUDA dependency is weakest and where hyperscalers have a vertical integration advantage. On current trajectory, Amazon is better positioned than Google to capture that share, which has implications for the AWS margin profile and the broader ASIC investment thesis without threatening our Nvidia view.